We know that a random variable distribution must satisfy the fundamental probability density function (PDF) requirements for a continuous random variable:

f(x)≥0, for all x∈R

∫−∞∞f(x)dx=1

P(a<X<b)=∫abf(x)dx

These conditions ensure that the function is a valid probability model over the continuous sample space.

To prove that the total area under the normal distribution curve is equal to 1, we evaluate:

P(−∞<X<∞)=∫−∞∞f(x)dx

Substituting the normal distribution PDF:

=∫−∞∞σ2π1e−2σ2(x−μ)2dx

Standardization Transformation

Let:

z=σx−μ

Then:

x=σz+μdx=σdz

Substituting:

=∫−∞∞σ2π1e−2σ2(σz+μ−μ)2σdz

Simplifying:

=∫−∞∞2π1e−2z2dz=2π1∫−∞∞e−z2/2dz

Relating to the Gaussian Integral

Recall:

∫−∞∞e−y2dy=π

To match this form, let:

y=2z

Then:

z=2ydz=2dy

Substituting:

=2π1∫−∞∞e−(2y)2/22dy

Simplifying:

=π1∫−∞∞e−y2dy

Using the Gaussian integral result:

=π1⋅π=1

Final Result

P(−∞<X<∞)=∫−∞∞f(x)dx=1

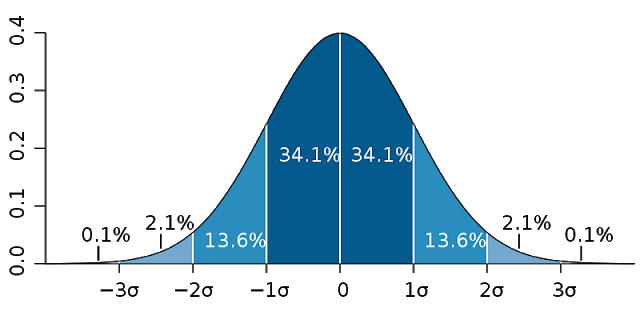

Thus, it is proven that the total area under the normal distribution curve is exactly 1, satisfying the fundamental requirement of a valid probability density function.